Borrower-Based Instruments

In January 2018, amendments to the Central Bank Law were adopted, establishing the legal framework for the Bank of Mongolia to implement macroprudential policy and creating the legal basis for introducing income-based credit restrictions, a cap on the credit that banks can lend to borrowers relative to their income.

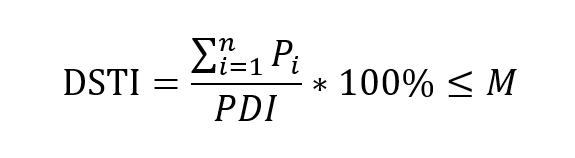

Debt-Service-to-Income Ratio (DSTI)

Within the macroprudential policy framework, DSTI limit has been set for consumer loans issued by banks and has been enforced since 2019. It indicates the maximum percentage of a borrower’s monthly income that can be allocated to servicing debt payments.

The DSTI ratio is a borrower-based instrument aimed at protecting the stability of the entire financial system, not just a single institution. Specifically, macroprudential policy instruments are designed to limit systemic risks that arise in real estate and credit markets.

The DSTI ratio is calculated in accordance with the “Methodology for Calculating the Borrower’s Debt-to-Income Ratio” approved by the Bank of Mongolia Governor.

- M – DSTI limit set by the Bank of Mongolia

- Pi – Monthly loan repayment calculated in accordance with clause 3.1 of the Methodology

- n – Number of loans excluding pension and herder’s loans

- PDI – Monthly personal income after tax calculated in accordance with clause 2.2 of the Methodology

Loan-to-Value Ratio (LTV)

The Loan-to-Value Ratio restriction is a limit on the amount of credit that banks can lend to mortgage borrowers, expressed as a percentage of the appraised market value of the real estate offered as collateral. The LTV for mortgage loans is set in accordance with the “Regulation on Mortgage Loan Operations” and the “Regulation on Housing Mortgage Financing” approved by the Bank of Mongolia Governor.

Consumer Loan Maturity Limit

In order to maintain consumer loan growth at an appropriate level, reduce household debt burdens, and prevent the accumulation of risks in the banking system, the Bank of Mongolia has set a 30-month maturity limit on consumer loans issued by banks — in addition to the DSTI limit — and this has been enforced since 2019.

Reserve Requirements

The reserve requirement (RR) requires banks to deposit a certain percentage of its funds collected from others in their current account at the Central Bank. This instrument is used not only to ensure banks’ liquidity and to manage money supply as part of monetary policy, but also within the macroprudential policy framework.

The Monetary Policy Committee of the Bank of Mongolia discusses and sets the RR ratio. The RR for tugrik and foreign currency funds had previously been set at identical rates, but as part of the macro-prudential policy, it has been set differently since 2018. This is a key policy instrument for preventing systemic risk accumulation, implemented under the following sub-objectives:

- to reduce banks’ incentive to secure riskier sources of funding, taking into account the nature of systemic risks;

- to manage the credit cycle — i.e., to smooth credit cycle.

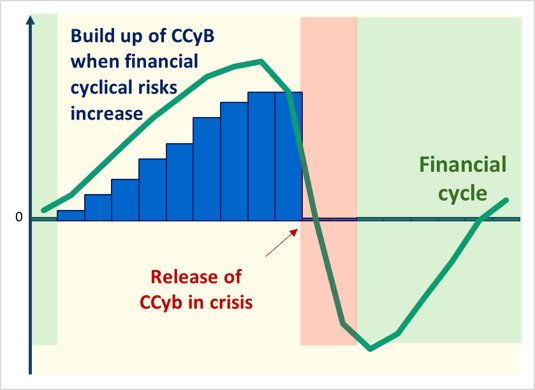

Countercyclical Capital Buffer (CCyB)

In 2010, the Basel Committee on Banking Supervision introduced the Basel III standards with the aim of strengthening the resilience of banking systems worldwide. Building on the lessons of the 2008–2009 global financial crisis, these standards incorporate the Countercyclical Capital Buffer (CCyB) — one of the key macroprudential policy instruments for ensuring financial stability. This instrument is designed to maintain the stability and resilience of the financial system throughout the credit cycle — in other words, to dampen procyclical fluctuations in the financial system.

The key feature of this instrument is that during periods of financial cycle overheating, financial regulators can increase capital requirements for banks, compelling them to build additional buffers and thereby improving their loss-absorbing capacity. Conversely, when stress emerges in the financial sector, these buffers can be drawn down to support the banking system’s operations, prevent disruptions to credit supply, and reduce adverse spillovers to the real economy.

Liquidity and Funding Instruments

Liquidity Coverage Ratio (LCR): In accordance with Basel Committee standards, a minimum LCR is set in order to determine and limit banks’ short-term liquidity risk. In other words, it is a regulatory standard that monitors whether banks maintain adequate liquidity in the event of sudden stress or a crisis.

Net Stable Funding Ratio (NSFR): In accordance with Basel Committee standards, the NSFR is used to manage and monitor banks’ long-term liquidity risk. This instrument encourages banks to fund their assets with sufficiently long-term and stable funding sources and prevents the creation of excessive maturity mismatches between assets and liabilities.